BILL MCDONALD:我很好,谢谢。很高兴再次与你交谈。这不仅仅是 Suncorp 的问题,是吗?此类骗局正在全国范围内袭击企业及其客户。人们如何做才能防止成为他们的目标?

ANNA BLIGH:嗯,你完全正确,Bill。这些骗局袭击了澳大利亚各地的人们,无论他们使用谁的银行或使用哪家电话公司,这些都是极其复杂的操作。我认为我们有时会认为诈骗者是一些业余爱好者,他们围坐在他们的车库里,试图,你知道,打击某人。实际上,他们是非常老练、有组织的犯罪团伙,经常在其他国家活动。他们有整个呼叫中心的人,他们每天的工作就是试图在你的盔甲上找到一个缝隙。

比尔·麦克唐纳:是的,这很可怕。我说的是澳大利亚银行业协会的首席执行官 Anna Bligh。快点,银行正在尝试做些什么来进一步防止这些骗局以保护客户?

ANNA BLIGH:好吧,每家银行都在为他们的网络安全投资数百万美元。曾几何时,银行花了很多钱建造巨大的铁金库,在那里他们可以锁上门并确保您的实物资金安全。如今,我们没有那种金库来保护我们的资金安全,我们有非常非常复杂的网络安全系统来保护我们的财务。

所以每一天,银行,有趣的是,许多银行现在都在雇佣更多的人——他们雇佣了更多的软件工程师、编码员和 IT 专业人员,而不是一线出纳员,因为那是他们需要投资的地方,这就是我们需要他们投入资金的地方。我认为让人们知道的另一件事非常重要的是,当事情发生时,当银行发现影响其客户的骗局时,他们确实有一个非常好的系统让彼此知道,所以如果事情发生在一家银行,其他每一家银行肯定能很快发现。所以他们分享这些信息。没有人认为这有任何竞争优势。如果一家银行被骗了,他们很快就会知道它会顺着他们的路走下去。

Determinants of Financial Literacy and Financial Inclusion in North-Eastern Region of India: A Case Study of Mizoram

by

Bhartendu Singh1 Raj Rajesh Ramesh Golait K. Samuel L.

Abstract

The present study evaluates the determinants of the status of financial inclusion and financial literacy in the under-banked North-Eastern Region of India based on field survey-data in the State of Mizoram. The survey indicated that there was limited financial awareness in the study region, about 32 per cent of the respondents were not aware of any financial products except the savings bank account. About 20 per cent of the respondents reported lack of knowledge of the basic payment options and about 43 per cent of the respondents reported knowledge but lack of usage of these options. About half of the respondents were found to be unaware of the financial institutions other than banks, viz., non-banking financial companies, microfinance institutions and small finance banks. It was also found that use of life insurance products was low among respondents. The financial inclusion score and financial literacy score for the study region were generated using the OECD/INFE (Organisation for Economic Co-operation and Development/ International Network on Financial Education) Toolkit for measuring financial literacy and financial inclusion. The average financial literacy score estimated in the study was 14.37 on a scale of 0 to 21 (i.e., 68.43 per cent) and the average financial inclusion score was 3.35 on a scale of 0 to 7 (i.e., 47.86 per cent). Several factors based on the literature were identified and tested in terms of their effect on financial inclusion and financial literacy using suitable econometric techniques, including a logistic regression framework. Among the identified factors, the place of residence (block), employment type and nature of family (joint versus nuclear) of the respondents were seen to strongly influence their financial inclusion and financial literacy status.

JEL Codes: G2, G18, G29, G21, G23

Keywords: Financial institutions and services, government policies and regulations, banks, financial institutions

Acknowledgement

The authors are profoundly grateful to the Local Board for Eastern Area, RBI for conceptualisation of the study. The authors take this opportunity to extend their thanks to the participants of the Department of Economic and Policy Research (DEPR) Study Circle seminar of RBI for useful comments on an earlier draft of the study. Authors are also grateful to an anonymous external referee for very detailed suggestions and generous comments on the study. The authors would also like to thank Dr. Deba Prasad Rath, Principal Adviser, DEPR for insightful suggestions and encouragement. Authors would also like to thank Dr. Pallavi Chavan, Director, DRG, DEPR, and her team members for their comments and support throughout the study. Nonetheless, the views expressed in this study are those of the authors alone and not of the organisations they are attached to. The authors only are responsible for errors and omissions, if any.

Bhartendu Singh Raj Rajesh Ramesh Golait K. Samuel L.

Executive Summary

Financial inclusion relates to the access to financial products and services. It is not limited to the basic access to deposits, but extends to the access to various financial services, including investments, credit, payments and insurance. Financial literacy provides basic knowledge and skills to analyse and understand financial products and services and assists in taking informed financial decisions. Financial inclusion without financial literacy may lead to exploitation as consumers may not be in a position to choose the right products and may end up taking uninformed decisions. On the other hand, financial literacy without financial inclusion is akin to providing skills without an opportunity to apply the same. In the long run, however, financial literacy takes people closer towards financial inclusion as there is a high likelihood that an aware person will seek access to finance and also achieve it.

Against this backdrop, the present study was conceived to look into various factors impacting financial literacy and financial inclusion in the north-east taking Mizoram as the site of the study. The study is based on primary data collected through a structured questionnaire. Total 523 respondents were selected from eight blocks, covering four districts, of Mizoram. The factors2 identified for the study are based on extensive review of the literature and the existing financial situation in Mizoram.

The survey indicated that there was a limited financial awareness in the study region. About 32 per cent of the respondents were not aware of any financial products except the savings bank account. About 20 per cent of the respondents reported lack of knowledge of the basic payment options and about 43 per cent of the respondents reported knowledge but lack of usage of these options. About half of the respondents were found to be unaware of the financial institutions other than banks, viz., non-banking financial companies, microfinance institutions and small finance banks. It was also found that use of life insurance was low among respondents.

The financial inclusion score and financial literacy score for the study region was generated using the OECD/INFE (Organisation for Economic Co-operation and Development/ International Network on Financial Education) Toolkit for measuring financial literacy and financial inclusion. The average financial literacy score estimated in the study was 14.37 on a scale of 0 to 21 (i.e., 68.43 per cent). The average financial inclusion score was found to be 3.35 on a scale of 0 to 7 (i.e., 47.86 per cent).

Out of 27 factors considered for the study as possible determinants of financial inclusion and financial literacy, the place of residence (block) was found to have large effect on both. Besides this, the type of employment and type of family (joint versus nuclear) also moderately influenced financial literacy. The subjects studied by the respondents as part of academic curriculum were also found to have moderate effect on financial inclusion. The financial literacy and financial inclusion were found to have a negligible effect on each other.

The relatively lower level of economic development, particularly financial development in the north-eastern region (NER), as reflected in relatively lower credit intermediation, is a major concern from policy perspective. In this context, the study highlights the need to conduct a greater number of financial literacy workshops, especially for the people belonging to the vulnerable groups at regular intervals in the region. Moreover, the development and outcome of such workshops need to be closely monitored by the funding agencies.

Determinants of Financial Literacy and Financial Inclusion in North-Eastern Region of India: A Case Study of Mizoram

Introduction

Financial literacy provides basic knowledge and skills to analyse and understand financial products and services and assists in taking informed financial decisions. Financial inclusion relates to the access to financial products and services. It is not limited to the basic access to deposits, but extends to the access to various financial services, including investments, credit, payments and insurance. Financial inclusion without financial literacy may lead to exploitation as consumers may not be in a position to choose the right products and end up taking uninformed decisions. On other hand, financial literacy without financial inclusion is akin to providing skills without an opportunity to apply the same. In the long run, however, financial literacy takes people closer towards financial inclusion as there is a high likelihood that a financially aware person will seek access to finance and also achieve it.

The Organisation of Economic Cooperation and Development (OECD) defines financial literacy as a combination of financial awareness, knowledge, skills, attitude and behaviour necessary to make sound financial decisions and ultimately achieve individual financial well-being. People achieve financial literacy through a process of financial education. According to the Reserve Bank’s ‘Committee on Financial Inclusion’ (Chairman: Dr. C. Rangarajan) (RBI, 2008), financial inclusion is the process of ensuring access to financial services, timely and adequate credit for vulnerable groups such as weaker sections and low-income groups at an affordable cost.

Financial literacy and financial inclusion are associated with each other. While there may be a positive correlation between the two, it is interesting to know if these two share a causal relation. It has been found in few studies that people who are financially included are not necessarily financially literate and many otherwise financially literate people are actually not financially included. Different studies in different places have arrived at contradictory findings, like there are studies which concluded that financial education results into higher savings for an individual in his/her lifespan later (Bernheim et al., 1997; Lusardi, 2003). However, some other studies could not find conclusive evidence that financial education improves personal financial decisions (Mandell, 2006; O’Connell, 2008). In the light of these contradictory results, it is interesting to know the other factors that have positive or negative impact on financial inclusion and financial literacy.

The North Eastern Region (NER) of India, comprising eight States namely, Arunachal Pradesh, Assam, Manipur, Meghalaya, Mizoram, Nagaland, Tripura and Sikkim, is characterised with a unique socio-cultural segment and predominantly semi-urban and rural areas encompassing hilly geographic terrain. The NER, home to 3.8 per cent of the national population, occupies about 8 per cent of India’s total geographical area, and is strategically important with over 5,300 km of international borders. Economic activity and banking parameters of the NER States, however, have remained unfavourable vis-à-vis all-India figures. At the same time, there remains a significant diversity in the level of development among the north-eastern States.

The Government of India, Reserve Bank of India and the respective State governments have been making special efforts for an all-round development of the region. Recognising the critical role of financial sector in economic development, and to investigate the issues limiting the success in achieving financial inclusion in NER, the Reserve Bank constituted a committee on ‘Financial Sector Plan for NER’ (Chairperson: Smt. Usha Thorat, 2006). Further, to address the issues related to development of the Micro, Small and Medium Enterprises (MSMEs) sector in NER, a separate sub-group was constituted under the Prime Minister’s task force on MSMEs (Chairman: Shri T.K.A. Nair) in 2009.

It was also emphasised in the literature that financial inclusion and development of NER holds the key to balanced regional economic prosperity (Rajan, 2016). The relatively low level of economic development, in general, and financial development in particular, of NER, as reflected in relatively lower credit intermediation, is a major concern from policy perspective.

In this context, the rest of the study is organised as follows: Section 2 lays out the objectives and rationale for choosing the State of Mizoram for the study. Section 3 highlights the socio-economic profile of the State. Section 4 presents the literature review. Section 5 provides the banking landscape of Mizoram economy. Section 6 presents empirical results and Section 7 concludes the study.

2. Objectives and Rationale for Choosing Mizoram for the Study

The objectives of this study are set out as follows:

To understand the architecture and ecosystem of Mizoram’s economy using secondary data;

To estimate the financial inclusion score of the State;

To analyse the factors, which determine financial inclusion in the State;

To estimate the level of financial literacy in the State;

To analyse the factors, which determine financial literacy in the State;

To assess public awareness about various government schemes (such as Direct Benefit Transfer (DBT), Pradhan Mantri Mudra Yojana (PMMY), PM Jan Dhan Yojna (PMJDY), etc.).

As per CRISIL (2018) Inclusix Score, North East Region (NER) is the least financially included region of India. Mizoram stood 31st among all the States in India by CRISIL Inclusix Score, though it is one of the most urbanised States of India. At the time of the survey conducted by CRISIL, out of eight districts, seven were ranked below 440 among all the districts of India. The capital of the State, Aizawl, stood at 294th in rank.

Interestingly, Mizoram is found to enjoy high branch penetration and above-average credit and deposit penetration as compared to other States. Further, as per the Census of India 2011, it is the second-most literate State in India whereas as second-least financially literate State as per National Centre for Financial Education Report, 2013.

The banking development in NER, including Mizoram, is a phenomenon post-bank nationalisation in 1969. Prior to it, no bank branch of commercial bank existed in Mizoram. In the year 1972, when it was accorded the status of a Union Territory, the whole of the State was served by a single branch of State Bank of India (SBI). Even today, the banking penetration remains highly skewed in terms of location. Furthermore, unlike other States, only one regional rural bank (RRB) serves whole of the State.

The studies focusing on financial inclusion and financial literacy in the State are less in number. All these aspects make the State an interesting case study to understand the factors influencing financial inclusion and financial literacy in a hilly State with a difficult geographical terrain.

3. Socio-Economic Profile of Mizoram

The State is situated in the southern corner of NER. The word ‘Mizoram’ is a combination of two words of local language, viz., Mizo and Ram. The word “Mizo” means ‘native inhabitants’ while “Ram” means ‘land’, thus “Mizoram” means ‘land of the Mizos’. It was known as Lushai Hills District of Assam till 1954 and then was renamed as Mizo Hills District of Assam until 1972, when it was carved out and given the status of a Union Territory. It continued as a Union Territory until 1987, when it was declared as the 23rd State of India on February 20, 1987 by the 53rd Amendment of the Indian Constitution.

3.1 History and Geography of Mizoram

Mizoram is a land-locked State sharing its borders with three Indian States, viz., Tripura (277 Kms) in the northwest, Assam (123 Kms) in the north and Manipur (95 Kms) in the northeast. It shares its boundary with two neighbouring countries, viz., Myanmar (404 Kms) in the east and south and Bangladesh (318 Kms) in the west. It had three districts when it was given the status of a State (1987), viz., Aizawl, Lunglei and Lawngtlai. In the year 1998, five new districts were created, viz., Kolasib, Mamit, Serchhip, Champhai (carved out of Aizawl) and Saiha (carved out of Lawngtlai). Recently on June 03, 2019, three new districts were added, viz., Hnahthial (carved out of Lunglei), Khawzawl (carved out of Champhai) and Saitual (carved out of Aizawl and Champhai).

About 95 per cent of population in State is of diverse tribal origins, mostly from Southeast Asia, who were settled over waves of migration since 16th century but mainly in 18th century. It has the highest concentration of tribal people among all States in India, and they are currently protected under the Indian constitution as a Scheduled Tribe. The tribes adopted Christianity over the first half of 20th century. Now, it is one of the three States of India with a Christian majority (87 per cent). Its people belong to various denominations, mostly Presbyterian in north and Baptists in south.

It is a highly literate agrarian economy; however, it suffers from slash-and-burn jhum or shifting cultivation, and poor crop yields. In recent years, the jhum farming practices are steadily being replaced with a significant horticulture and bamboo products industry. The State has about 871 kilometres of national highways, with NH-54 and NH-150 connecting it to Assam and Manipur respectively. It is also a growing transit point for trade with Myanmar and Bangladesh. It is a land of rolling hills, valleys, rivers and lakes. As many as 21 major hill ranges or peaks of different heights run through the length and breadth of the State. As per the State of Forest Report, Mizoram has the highest forest cover as a percentage of its geographical area, i.e., 84.5 per cent.

The fabric of social life in the Mizo society has undergone tremendous changes over years. Before the British moved into the hills, the village and the clan formed units of Mizo society for all practical purposes. Mizos are giving up their old customs rapidly and adopting new modes of life, which is greatly influenced by the western culture. Many of their present customs are mixtures of their old traditions and western pattern of life.

3.2 Architecture of the Mizoram Economy: A Sectoral Analysis

In line with the trend in structural shift in other States, the share of agriculture has declined and the share of industry and services sector in gross state value added (GSVA) has picked up (Chart 3.1). Within the agriculture sector, ‘forestry and logging’ (accounting for more than half of the agriculture and allied sector) dominates and its share has expanded in the last couple of years with a corresponding shrinkage in the share of crops, livestock and fishing and aquaculture (Chart 3.2). Mizoram is richly endowed with bamboo forests, which broadly cover half of the State’s land. It has the largest bamboo cover as a proportion of its geographical area in the country. It produces a variety of bamboo-based handicraft products and exports bamboo and teak wood to Bangladesh. The handloom production, estimated to be Rs.6 crore, generates several non-farm employment. It has great potential for export under the Look East Policy of the Government of India, given the similarity of fabrics being worn by the inhabitants of the South East Asian countries as produced by local weavers of the State.

In line with the all-India trend, despite the decline in the share of agriculture in GSVA, the State economy is primarily agrarian with 60 per cent of the population depending, directly or indirectly, on agriculture. Rest of the working population is engaged in government jobs, small businesses and transport activities. Within the industrial sector, ‘electricity, gas, water supply and other utility services’ dominates with 56.4 per cent share in the industrial sector followed by ‘construction’ with 39.8 per cent share in 2019-20 (Chart 3.3). Manufacturing constitutes around 0.7 per cent of the GSVA, while mining constitutes around 0.3 per cent of GSVA.

Within the industrial sector, the share of manufacturing, mining and construction has been shrinking in the last couple of years, while that of ‘electricity, gas, water supply and other utility services’ has been expanding. As per the sectoral composition, services sector activity dominates the State economy as it accounts for nearly half of the GSVA (Chart 3.4). The service sector is dominated by public administration, which constitutes around 30 per cent of the services sector followed by trade, repair, hotels and restaurants.

The overall GSVA growth in the State has been highly volatile in line with the growth of the constituent sectors, which have exhibited marked year-to-year variation (Chart 3.5). Mizoram remains distinct from other north-eastern States in terms of economic development, the second highest per capita income followed by Sikkim in the NER. In line with its elevated level of per capita income, its poverty level is lower than the national average (Chart 3.6).

3.2.i Agriculture

Agriculture is the mainstay of the people of Mizoram (Savant and Patnaik, 1998). About 90 per cent of the farmers in the State are small and marginal farmers3. The average size of land holding of the farmers is 1.25 hectares.

Jhum or shifting cultivation is the main agricultural practice and it is carried out annually by a large number of people living in rural areas. The productivity of this type of agriculture is comparatively lesser than the national average. The performance of area, production and yield of major food-grains in the State suggests a mixed trend (Chart 3.7). Rice, coarse cereals and pulses are the main crops.

Food grain production, at 76.9 thousand tonnes (in 2019-20), is the least amongst the NER States. It constituted merely one per cent of the total food grain production of the region. The State has total geographical area of 2,108,700 ha of which net sown area is 218,608 ha (10.4 per cent of total geographical area). The average of gross and net sown area for the last five years in Mizoram has changed in tandem with NER (Chart 3.8).

Net irrigated area in the State is 18,813 ha, which is just 8.6 per cent of total sown area. Major and medium irrigation is a challenge due to the hilly terrain. Although Mizoram receives sufficient rainfall during monsoon, only small areas of fertile land can be brought under cultivation during rabi season due to lack of enough water harvesting structures. Concerted efforts are required to increase soil moisture retention capacity, create irrigation facilities like tube wells, rainwater-harvesting structures and other water bodies for life saving irrigation during dry season. The State is blessed with an abundant rainfall, but its porous soil and inadequate irrigation infrastructure has affected its crop yield. The yield issue can be addressed by creating irrigation infrastructure and adoption of better crop technologies. Chart 3.9 shows that the State also has very low consumption of fertilisers and pesticides.

Farm mechanisation on an extensive scale is not feasible in the State due to hilly terrain, limited flat land, fragmented land holdings and poor road connectivity. Consequently, use of tractors and power tillers, adoption of new cropping pattern and efficient utilisation of available irrigation facilities are not being utilised at desired level for increasing the agricultural production in the State.

Given the by and large subsistence nature of farming, the requirements of credit by agricultural households are meagre. As per the NSSO’s survey, agricultural households in Mizoram met about 86 per cent of their loan needs from institutional sources (Chart 3.10). This contrasts with some of the other NER States such as Manipur wherein the informal sources formed a significant chunk of credit (Chart 11).

Measuring Contagion Effects of Crude Oil Prices on Sectoral Stock Price Indices in India

Madhuchhanda Sahoo, Arvind Kumar Shrivastava, Jessica Maria Anthony and Thangzason Sonna@

Abstract

1This paper explores the contagion effects of extreme changes in global crude oil prices on sectoral stock price indices in India. Using generalised Pareto distribution (GPD) for estimating excess returns or exceedances i.e., deviations from thresholds, and multinomial logit model (MNL) for assessing the probability of contemporaneous excess returns or co-exceedances, the paper finds a significant likelihood of co-exceedances among 10 sectoral stock price indices when faced with extreme changes in global crude oil prices. This points to the existence of a contagion effect. The evidence of positive co-exceedances is stronger, and the results are found more robust when relevant control variables are introduced – exchange rate returns (INR-USD), 10-year G-sec yield, and differential stock returns, (i.e., small firms minus big firms (SMB)). The contagion effect on all sectoral indices, irrespective of their direct and indirect exposure to oil price dynamics, highlights the need for hedging by investors as mere diversification of portfolios may not be sufficient to protect their assets from an adverse oil price shock.

The studies on contagion effects of extreme changes in global prices of crude oil on sectoral stock indices done in the Indian context are rare. There are not many studies on this subject even at the international level. The increasing cross-border financial integration warrants that the contagion effects of global prices of crude oil – one of the most actively traded commodities worldwide – on stock prices is understood better. For an oil-dependent economy like India, importing around 80 per cent of its consumption requirements, the need for a deeper understanding of the contagion effects of global crude oil prices is all the more pressing.

Oil has both commodity and financial attributes. As a commodity, while rising oil price increases the operating costs of firms leading to depressed stock prices, as a financial asset, when higher oil price is driven by higher demand expansion, it positively affects stock returns. Studies have observed that crude oil shocks can influence expected earnings in the equity markets, both within and across borders, while the macroeconomic impact of oil price shocks can also have ramifications for overall liquidity in the financial market.

Commensurate with being the second-largest country in the world in terms of population, the fifth-largest economy in the world, and third in Asia, India holds the distinction of being the third-largest consumer of oil, next only to China and the US. Likewise, India is the third-largest importer of crude oil after the US and China. Domestically, oil is the largest source of the country’s total energy supply next only to coal and also is the largest in terms of total final consumption. The demand for oil is increasing rapidly. Yet, owing to low natural endowment and stagnant domestic production, India’s reliance on imports for meeting the demand-supply gap is high. Also, the oil and gas sector is one of the six core industries in India and is among the most traded commodities. It is, therefore, natural that the implications of extreme changes in global prices of crude oil on the Indian macro economy would be profound. In the same vein, it may not be farfetched to expect movements in global prices of crude oil to impact Indian stock indices. More so because the Indian stock market has grown larger, and the Indian financial system is substantially integrated with the global financial system over the years.

In this backdrop, with the motivation to empirically examine the existence of contagion effect of extreme changes in global crude oil returns on 10 composite sectoral indices of Indian stock markets, the paper employs the multinomial logit model (MNL), as in Sheng Fang and Paul Egan (2018) for China. The threshold returns for global crude oil price and sectoral stock indices – both for the top and bottom tails, are established using a generalised Pareto distribution (GPD) function. Having established the thresholds, the MNL model is used to examine the probability of extreme returns or exceedances, defined as deviation from thresholds, contemporaneously occurring among the stock sectors due to exceedances in oil price returns, which the literature has defined as contagion effects.

The study has been organised into five sections. Section II presents the review of the literature and the stylised facts. Section III provides a detailed explanation of methodology, data, and preliminary analysis. Section IV reports and analyses the empirical results and Section V concludes the paper.

II. Review of Literature and Stylised Facts

II.1 Review of Literature

Hamilton (1983) discovered that crude oil price changes played a key role during every post-World War-II US recession. After his pioneer work, exploring the linkages between crude oil price and the real sectors of the economy has been a major area of theoretical and empirical research. Successive researchers investigated the association between oil price shocks and macroeconomic variables – economic growth, aggregate demand, inflation, and employment in various countries. The subsequent studies that followed, established without ambiguity that oil price shock has the potential to trigger cost-push inflation, adversely affecting profitability and causing generalised inflation. And if unchecked, it can engulf the whole economy, leading to higher unemployment, compressed demand, and consumption, discouraging investment, and a sustained growth slowdown.

Indeed, the crude oil price surge due to the Arab oil embargo was at the core of the global slowdown during 1974-75. The global Gross Domestic Product (GDP) grew by 6.9 per cent in 1973, fell to 2.1 per cent in 1974, and to 1.4 per cent in 1975. It was only by 1976 after the oil embargo that the world economy returned to its normal rate of growth. The US GDP contracted for three consecutive years during 1973-75 and unemployment and inflation rates more than doubled. So pervasive was the impact that it led to an aspersion on the foundation of Classical Economics, according to which inflation is always and everywhere a monetary phenomenon, and its off-shoot – the Philips Curve – which assumed a steady, permanent, and direct relationship between employment and inflation.

The studies on the relationship between volatility in crude oil price movements and stock indices have been relatively of a new vintage as compared to studies on the relationship between crude oil price movements and macroeconomic variables. The premise that the rise in performance of the stock market is a good indicator of economic activity, has existed all along as a perceived notion. In fact, this notion led to another perceived notion of the existence of a causal relationship between crude oil price and the stock market. Studies like Nasseh and Strauss (2000); Pethe and Karnik (2000); Singh (2010); Dhiman and Sahu (2010) have attempted to empirically examine the relationship between crude oil price and macroeconomic variables in different countries including India. Most studies observed a strong relationship between crude oil price movements and macroeconomic variables.

As regards crude oil price movements and stock markets, the empirical literature has been vast, and the findings thereof point mostly to an inverse relationship. There have, however, been a few studies that have found the relationship to be non-existent as well. Commonly, the relationship between the two markets has been analysed using (a) extreme returns on crude oil price, frequent fluctuations in crude oil prices, the net external trading position of the country in the global crude oil market (exporter or importer), and origin of crude oil price shocks (demand or supply-driven) on the one hand, and (b) overall returns or volatility of stock markets on the other, with relevant control variables like foreign currency exchange rate and interest rate.

A study on stock markets of the Gulf Cooperation Council (GCC) pointed out that negative oil price change had a larger negative impact on the stock markets of Kuwait, Oman, and Qatar which being oil exporting countries are relatively more responsive to the considerable oil price change (IMF WP, 2018). The stock markets of Latin American countries have been found to respond positively to increases in oil prices during 2000-2015 (Salgado et al., 2017). According to the authors, their finding can be explained based on regional closeness, shared institutional, historical and cultural features, and the way country-funds and regional-funds managers and other institutional investors who hold Latin American stocks react to oil price shocks.

Examining the differential impacts of fluctuations in crude oil prices on oil-importing and exporting countries, Asteriou, Dimitras, and Lendewig (2013) observed that the impact was higher for countries importing crude oil than countries exporting it and that the relationship between oil price and stock markets was more robust than between various interest rates – both in the short and long-runs. Imarhiabel (2010) also examined the effect of crude oil prices on the prices of stocks of select major oil-producing and consuming countries such as Mexico, Russia, Saudi Arabia, India, China, and the United States, and detected that stock prices were affected by both oil prices and currency exchange rates. Further, a time-series study of almost three decades by Thorbecke (2019) highlighted that the US stock markets got negatively affected by shocks in oil price during 1990-2007, but after that, they were positively affected during 2010 to 2018 indicating a change in nature of the relation. This finding, according to the author was explained by the rise of shale oil production and the changed structure of US economy – stocks in many sectors that were harmed by oil price increases before the Shale revolution benefited in the latter period.

Even for India, the relationship between the two markets has been negative according to most studies. A study by Rai and Bairagi (2014) showed a significant correlation between a crude oil price change and Bombay Stock Exchange (BSE) Sensex for the period 2003 to 2012. Another study by Sathyanarayana et al. (2018) spoke of a positive, significant, and direct relationship between crude oil and BSE Sensex, with an increase in oil price leading to an increase in share market price. Fluctuations in crude oil price return exerted a significant impact on the volatility of stock market returns in India and such volatility spillovers were stronger following the global financial crisis (Anand et al., 2014).

But there have been exceptions. According to Chittendi (2012), volatile stock prices did not necessarily have a significant impact on oil price volatility and there was no long-run equilibrium relationship between international crude oil price and the Indian stock market during 2003 to 2011, although such a relation was observed during 2008-2011 (Ghosh and Kanjilal, 2016). Surprisingly, oil demand shocks, but not supply shocks, affected stock returns in India and its volatility, despite the fact that policy uncertainty could lead to negative returns and increased volatility (Anand et al., 2021).

Despite being a vastly studied topic, the precise relationship between crude oil price volatility and stock prices and the contagion effect thereof has not been stated with certainty. This has prompted a new approach to study the two markets i.e., to take into consideration industry-specific stock prices. The widely held view is that the sectoral segregation of stock market indices is necessary to gain a deeper knowledge of the impact of crude oil price fluctuations.

However, even in this regard, there have been not many studies in the Indian context. Studies exist for other countries, such as the US, Europe, and China. A study by Degiannakis et al. (2013) highlights the importance of the sectoral division of the stock market with regard to various industries as an important determinant in determining the nature of the association between prices of international crude oil and the stock market. They examine equity returns of 10 European industrial sectoral indices and their linkages with oil price changes via the Diag-VECH GARCH model and conclude that relationships are industry-specific. Another study on the relationship of European sectoral stocks with crude oil prices is found to be asymmetric (Arouri, 2011) and strongly varying across sectors. While Automobiles and parts, Financials, Food and Beverages, and Health care show a negative relationship, Oil and Gas show a positive relationship.

In another study by Thorbecke (2019), a positive relationship between crude oil price volatility and stock prices were seen for industries that acted as an input to the energy sector, such as industrial machinery and marine transport and industries in the oil supply chain (petrochemicals). Kang et al. (2017) concluded that the index for the oil and gas industry responded negatively to negative supply-side shocks and positively to positive aggregate demand shocks for the US.

It was also found that stock prices of manufacturing, chemical, medical, food, transportation, computer, real estate, and general services responded negatively to a rise in oil prices, whereas the results were indeterminate for stock prices of engineering, electricity, and financial sectors by using 56 firm-level stocks of the US (Narayan and Sharma, 2011). In one interesting time-series study by Singhal and Ghosh (2016), the relation of seven industry-specific sectoral stock prices of BSE with crude oil prices was examined and significant empirical evidence was obtained.

Yet in another study, Rajan and Lourthuraj (2020) have tried to understand the impact of crude oil price on the automotive sector and companies’ performances. Jambotkar and Anjana (2018) also through an empirical analysis studied the combined effects of macro-economic variables, including crude oil prices on selected National Stock Exchange (NSE) sectoral indices and found significant results. A recent paper by Fang and Egan (2018) investigated the contagion effects using extreme positive and negative returns and the multinomial logit model (MNL) for 10 Chinese stock sectoral indices. The theory of extreme value has been used the least to understand the oil price spill over on sectoral stock prices in the case of Indian stock markets. It was used only in a few other countries and other fields like Horvath et al. (2018) and Chan-Lau et al. (2012). In addition to this, the literature shows that very few studies exist on the impact of crude oil prices on cross-market linkage i.e., inter-sectoral linkage for extreme returns in crude oil prices for India’s stock markets.

Hence, a study of sectoral stock price indices and an attempt to measure inter-sectoral linkages are key to understanding the nature of the relationship between oil prices and industry-specific sectoral stock markets. This paper is a step in that direction.

II.2 Stylised Facts

The Indian stock market has grown significantly in the last two decades. The number of listed companies in the NSE is more than 1900 while its benchmark index, Nifty comprises 50 companies. The NSE also has many sectoral and thematic indices. Similarly, BSE’s Sensex is a weighted stock market index of 30 well-established listed companies. The BSE is among the world’s 10 largest exchanges in terms of the cumulative market capitalisation of all companies listed on its platform, as per the latest data available from the World Federation of Exchanges. The NSE has maintained the position of the largest derivatives exchange during 2019 and 2020 in terms of the number of contracts traded.

The BSE has the largest number of listed companies in the world (in the case of equities and debt). BSE is also the fastest exchange in the world with a median response time to trade of 6 microseconds. The NSE was by far the largest exchange in terms of stock index options trading, with over 1.85 billion contracts traded in H1 2019.

The average daily turnover in NSE was ₹57,677 crore and market capitalisation was ₹2,55,68,863 crore as on end-May 2022 and for BSE, the average daily turnover was ₹4,192.1 crore and the market capitalisation was at ₹2,57,78,368 crore in the same period. The stock market capitalisation to GDP ratio for BSE has improved significantly from 24 per cent in 1992-93 to 104.9 per cent in 2020-21.

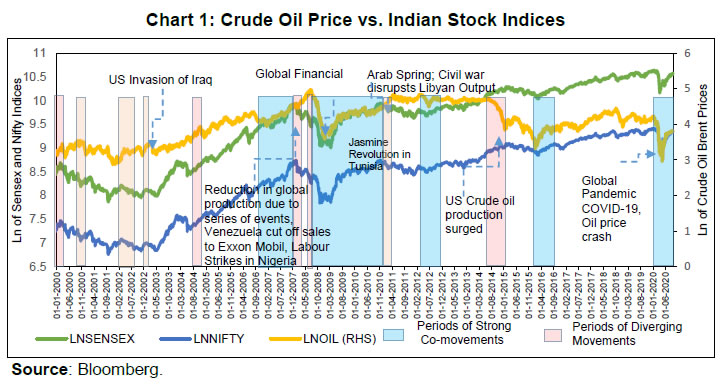

Apart from these milestones, the co-movement of Indian stock indices with global crude oil price (Brent) and these indices getting affected by major global events make it even more necessary to study the relationship between these indices and global crude oil price (Chart 1).

The contagion impact of global crude oil price on stock indices at the sectoral level is also backed by theory. There are two prominent theories supporting the linkage of international crude oil price movements and sectoral/industry-specific trends in stock indices. The first one, the channel of Expected Cash Flows states that the rise in oil prices leads to a rise in the cost of production, which in turn can reduce profit margins and hence cash flows (Dadashi et al., 2015). Theoretically, oil marketing, paints, synthetic rubber (tires), and the aviation industry’s input costs might rise due to a surge in crude oil price and their stock prices fall with rise in global crude oil price. Similarly, oil production and exploration companies may profit from a rise in crude oil prices and their stock prices may rise. The second theory of Discounted Future Cash Flows says that high oil prices can lead to inflationary expectations and hence rise in the interest rate, ultimately leading to higher borrowing costs.

The ultimate response of stock prices to crude oil price shocks, however, would depend upon whether the company is oil-producing or consuming. More importantly, the input-output coefficient of that sector would determine the responsiveness of its stock to oil price shocks. The volatility in oil prices can affect the operating costs of firms – both oil-producing and consuming and hit their earnings. Similarly, the profit and dividends of firms that use oil as inputs – direct or indirect, are bound to be impacted by volatility in oil prices. Likewise, the volatility in oil prices for an oil-importing or exporting market will differ widely. An upward movement in oil prices, while increasing risk and uncertainty in oil-importing markets, will increase market returns for an oil-exporting market. With a view to exploring these aspects of the behaviour of oil price movements on sectoral stock indices, 10 sectoral stock indices from BSE/NSE have been mapped against the input-output coefficient of India (MOSPI, 2012) taking petroleum products as the input. The input-output coefficients2 across eight sectors were estimated (Chart 2).

The higher input-output coefficients for Oil and Gas, and Basic Materials are on expected lines since the input intensity of petroleum products in these sectors is higher than in other sectors, such as IT and Financial Services. However, a broadly similar returns pattern can be observed across all stock sectors as well as Brent crude returns despite higher volatility in crude returns. All the 10 stock sector returns shared a statistically significant and positive correlation with Brent crude returns ranging between 0.11 to 0.20, indicative of the presence of contagion effect from extreme changes in global crude oil prices (Chart 3). Excessive volatility in oil price can affect expected earnings even for firms that are not related to oil directly thereby affecting equity prices.

III. Data and Methodology

III.1 Data and Preliminary Analysis

The time range for the paper is almost a decade and a half (14 years), from January 01, 2007 to December 08, 2020. The period has been chosen keeping in mind two aspects: a) the availability of data on most sectoral indices and b) the occurrence of two defining global crises of the century – the global financial crisis of 2008 and COVID-19 induced-recession of 2020. The data used are high-frequency daily data.

Most of India’s crude oil imports are from the OPEC countries and Brent is their benchmark index. Moreover, Brent is highly correlated with West Texas Intermediate (WTI). Hence, daily data on International crude oil prices (Brent) has been taken from Bloomberg. Sources of stock indices are Bloomberg and NSE and BSE websites. The Nominal Exchange rate (USD/INR) is obtained from RBI and the Financial Benchmarks of India Private Ltd. (FBIL). Data on the long-term interest rate (G-Sec 10-year yield) is collected from Bloomberg. The 10 sectoral stock indices used in the study are – Capital Goods (BSETCG), Consumer Durables (BSETCD), Basic Materials (BSESPBSBMIP), Oil and Gas (BSEOIL), Auto (NSEAUTO), Information technology (NSEIT), FMCG (NSEFMCG), Metal (NSEMETAL), Financial Services (NSEFIN) and Commodities (NSECMD). The rationale for the choice of above mentioned 10 sectors is based on their importance to the economy, extreme returns, and input-output coefficients (Chart 3); and weights in stock exchanges (market capitalisation) (Chart 4).

This paper estimates the tail risks of consumer price inflation in India using a quantile regression framework. It examines the impact of various domestic and global macroeconomic factors, along with the role of the flexible inflation targeting (FIT) in influencing the inflation tail risks as well as in explaining the shifts in its conditional distribution. A rise in domestic income and household inflation expectations, elevated global commodity prices – both fuel (i.e., crude oil) and non-fuel, and easy financial conditions pose upside risks to Consumer Price Index (CPI) headline inflation. The results also show that both lower and upper tail risks of inflation have stabilised in the FIT period and that the macroeconomic factors capture the tail risks to the inflation target band of 2 to 6 per cent in India reasonably well.

JEL Classification: C21, C53, E31, P24, P44

Keywords: Inflation at risk, inflation uncertainty, monetary policy

Introduction

A precise estimate of the future inflation path and uncertainties around it is crucial for a proper assessment of inflationary conditions. During extreme events, such as the global financial crisis (GFC) and the COVID-19 pandemic, it becomes very difficult to predict the trajectory of inflation due to uncertainties surrounding it. In such circumstances, the distribution of future inflation, in addition to the inflation forecast, may be useful for future guidance, particularly under a flexible inflation targeting (FIT) framework.

For India, food – a major component of the consumer price index (CPI) basket – typically has higher volatility owing to supply-side issues and the monsoon dependence of Indian agriculture. As a result, any disruption in weather patterns gets reflected in production, and in turn, prices. Extreme weather events namely, excess rains, deficient rains, floods, cyclones etc., bring additional uncertainty around the conditional mean trajectory of food inflation and makes it less reliable. Similarly, the high dependence of India on crude oil imports makes it susceptible to any global oil price shock.

The uncertainty around food price inflation spills over to the uncertainty around CPI headline inflation as food occupies a significant proportion of the CPI basket and is also susceptible to many supply shocks. In such times of uncertainty, along with the mean path of future inflation, the distribution of inflation becomes crucial in the assessment of inflationary conditions. The inflation distribution may help in a proper assessment of the upside and downside risks to inflation.

The upside and downside risks to inflation are known as Inflation at Risk (in notation, IaR) in the literature, a measure similar in notion and concept to Value at Risk (VaR) in financial risk-management theory to estimate the market and credit risk of a portfolio (Andrade, Ghysels, and Idier, 2012; Banerjee et al., 2020; López-Salido and Loria, 2020). The conventional approach assumes the symmetric distribution of errors around the mean path, which, however, may not always hold. Thus, the asymmetric nature of future inflation distribution may be useful in explaining the tail risks (i.e., the possibility of extreme values on either side) of inflation and in helping the monetary policy in communicating the balance of risks.

Besides the asymmetry, understanding and accounting for the uncertainty around the central tendency are also crucial in stabilising inflation. Inflation uncertainty is one of the primary costs of inflation to the real economy as expected inflation is an important factor while making economic decisions. Uncertainty surrounding future inflation creates uncertainty regarding the future value of savings and investments, which in turn, may distort the efficient allocation of resources (Chowdhury, 2014). Consequently, inflation uncertainty can adversely affect consumption, investment, and growth. Since the monetary authority’s primary objective is to stabilise prices, it is also crucial to empirically examine whether it accounts for inflation uncertainty in monetary policy formulation.

Given the importance of the distributional characteristics of inflation, the paper derives a conditional distribution of inflation which also indicates the balance of upside or downside risks. The paper has the following objectives:

Estimate tail risks of inflation in India corresponding to various domestic and global drivers and test whether inflation risks have stabilised in the IT period;

Examine shifting of the conditional distribution of inflation for different domestic and global shocks;

Estimate expected tail values of inflation and examine the robustness of the models;

Examine the causal relationship between inflation and inflation uncertainty and assess the reaction of the monetary policy to the asymmetric nature of conditional distribution and uncertainty around the central tendency.

Estimations of conditional distribution and tail risks are based on a hybrid version of the standard New Keynesian Phillips Curve (NKPC) framework with financial conditions, crude oil price, and exchange rate of the Indian rupee (INR) vis-a-vis US dollar (USD) and global demand conditions- proxied by US real GDP growth as additional explanatory factors (Auer, Borio, and Filardo, 2017). The paper also examines the role of the IT framework in stabilising the tail risks. Therefore, the study includes both demand and supply-side factors in the estimation of the conditional distribution. In the Indian context, the existence of the Phillips curve has been established based on samples at national as well as sub-national levels in the post-GFC period (2007-09) (Behera, Wahi, and Kapur, 2018; Salunkhe and Patnaik, 2019). In this regard, a recent study by López-Salido and Loria (2020) concluded that tail risks are sensitive to domestic economic slack and have a significant role in influencing inflation distribution. Some recent studies have also considered the financial conditions index to examine the upside and downside risks to inflation during tight/easy financial conditions (Chevalier and Scharfstein, 1996; Gilchrist, Schoenle, Sim, and Zakrajšek, 2017). Chevalier and Scharfstein (1996) argue that during tight financial conditions, firms that face a higher constraint on accessing liquidity may set a higher price to increase their cash flow leading to higher inflation.

India adopted the flexible IT framework in 2016, which was reviewed in March 2021, wherein the inflation target of 4 per cent with a ±2 per cent band around it was continued until the next review in 2026. During the period from 2011-12 to 2013-14, the average CPI-C inflation rate stood at 9.4 per cent, which moderated gradually towards the midpoint of the target band during the IT period. Notably, CPI-C inflation averaged 3.9 per cent during the IT phase of October 2016 – March 2020. RBI (2021) highlights the success of the framework in anchoring inflation expectations of both households and professional forecasters and lowering average inflation.

Given the relevance of inflation projections in policy formulations, the RBI regularly publishes a fan chart of asymmetric inflation distribution based on a two-piece normal distribution which consists of two normal distributions below and above the mean (Banerjee and Das, 2011). Both the pieces have the same mean, but different standard deviations. This difference in standard deviations brings the asymmetry of a distribution around the mean. In the two-piece normal distribution, the values of standard deviations are derived from the past deviations from the forecast values, which incorporates asymmetry in the distribution. However, this paper derives the conditional distribution of inflation based on the estimated quantiles from quantile regression conditioned on the macroeconomic environment rather than depending on the past. Few recent studies in advanced economy central banks have highlighted the usefulness of conditional quantile regression in deriving the fan chart by incorporating expert judgements (for instance, see Sokol, 2021). Therefore, deriving the conditional distribution of inflation based on the current macroeconomic situation rather than depending on the past as in the case of a fan chart is the major contribution of this paper.

The paper analyses the historical tail risks and shifts in the conditional distribution of inflation for various shocks. It concludes that a rise in domestic income and household inflation expectations increases the upside risks and lowers the downside risks to inflation. Elevated global commodity prices of both fuel (i.e., crude oil) and non-fuel, global economic growth and easy financial conditions raise the upside risks to inflation. Further, the results add to the success story of the adoption of the IT framework in India in stabilising CPI headline inflation as both lower and upper tail risks of inflation have stabilised in the IT period. Regarding the predictive efficiency of the models, the paper concludes that the models based on various macroeconomic factors capture the tail risks to the inflation target band of 2 to 6 per cent in India to a considerable extent. While examining the response of the monetary policy to asymmetry and uncertainty of inflation distribution, the paper finds evidence of tightening of the monetary policy during the periods of higher inflation uncertainty.

The rest of the paper is organised as follows. Section II discusses the literature on the conditional distribution and tail risks associated with CPI-C inflation in India. Building on the literature and existing data sets, Section III presents a few stylised facts for inflation in India during the sample period and discusses the methodology used in the paper. Section IV presents the empirical results and also examines the asymmetry and uncertainty pertaining to inflation distribution and the response of the monetary policy to these. The last section concludes the paper with a few policy implications.

II. Literature Review

Studies that focus explicitly on the analysis of tail risks of inflation are relatively new in the literature (Banerjee, Contreras, et al., 2020; López-Salido and Loria, 2020). However, a few studies in the last decade analyse the quantiles of inflation and their dynamics; for instance, Wolters and Tillmann (2015) examine the persistence of different quantiles in the conditional distribution of inflation. Gupta, Jooste, and Ranjbar (2017) find higher persistence of inflation for higher quantiles in the case of South Africa. In related literature on convergence, Tsong and Lee (2011) in a study of 12 OECD countries find asymmetric convergence of inflation to long-run value post negative and positive shocks using the quantile regression approach. They find that positive shocks are more persistent than negative shocks and converge slowly to the long-run level. Similar empirical evidence is also seen in Uganda (Anguyo, Gupta, and Kotzé, 2020).

Several studies have focussed on various determinants of inflation in a quantile regression framework; for instance, Iddrisu and Alagidede (2020) explain food inflation and its various determinants, such as economic growth, world food price inflation, monetary policy, etc., using quantile regression for South Africa. Lahiani (2019) explores the transmission of crude oil prices to different quantiles of overall prices for the US.

Further, a plethora of studies have focused on the important determinants of conditional mean inflation using Phillips-curve specification and its different versions. Many of these studies find that the Phillips curve relationship estimated at the mean level weakened after the GFC (Blanchard et al., 2015). A few studies extend the NKPC estimation by incorporating global economic slack along with domestic economic slack to explain the domestic inflation dynamics (Auer, Borio, and Filardo, 2017). However, the evidence of global economic slack is mixed. For instance, Forbes (2019) finds significant evidence of the role of global economic slack on domestic inflation, while Mikolajun and Lodge (2016) find a limited impact of it on domestic inflation. Xu, Niu, Jiang, and Huang (2015) use non-linear quantile regression to estimate the Phillips curve for the US and conclude that the shape of the Phillips curve differs across quantiles. In the case of India, researchers find evidence for the existence of the Phillips curve based on samples from national and sub-national data in the post-GFC period (2007-09) (Behera, Wahi, and Kapur, 2018; Salunkhe and Patnaik, 2019).

The above studies focus on exploring quantiles of inflation and do not explicitly mention the tail risks of inflation. Andrade et al. (2012) introduced an explicit analysis of tail risks of inflation i.e., “Inflation at Risk (IaR)” and used asymmetric property and distributional uncertainty to explain the monetary policy rule. The tail risks of inflation have been a major concern, particularly in advanced economies, in the post-GFC period (López-Salido and Loria, 2020).

Some recent studies have also considered the financial conditions index to examine the upside and downside risks2 to inflation during tight/easy financial conditions (Chevalier and Scharfstein, 1996; Gilchrist, Schoenle, Sim, and Zakrajšek, 2017). Firms facing higher constraints on accessing liquidity during tight financial conditions and firms with weak balance sheets may set a higher price leading to higher inflation. In a recent study, Banerjee et al. (2020) use the volatility of asset prices as a proxy for tight financial conditions and find a significant impact of financial conditions on inflation. Some earlier studies based on quantile regression also find a positive association between stock market return and different quantiles of inflation in G7 countries (Alagidede and Panagiotidis, 2012).

Inflation at Risk is similar to the concept of Value at Risk (VaR) in financial risk management, i.e., the extreme quantiles for a given level of probability. Among macroeconomic variables, a similar measure is also available for economic growth as Growth at Risk (Prasad et al., 2019). López-Salido and Loria (2020) in their study of advanced economies explicitly derived the conditional distribution based on quantiles. Banerjee et al. (2020) extended the analysis by including emerging economies and estimated the conditional density. Their study concludes that countries with IT show a relative moderation in inflation risks than non-IT countries. Banerjee, Mehrotra, and Zampolli (2020) model the impact of the COVID-19 pandemic and find higher upside and downside risks to inflation in emerging economies, and higher downside risks in the case of advanced economies.

The advancement in deriving the conditional distribution based on quantile is a novel contribution in the above studies as compared to earlier studies that used quantile regression to study the quantiles of inflation and their dynamics. These studies highlight, in particular, the impact of different shocks on the tail risks of inflation. In our analysis, we augment the above-discussed analysis for India and examine certain country-specific features to explain the dynamics of tail risks of inflation.

In related literature, Andrade et al. (2012) examine the response of the monetary policy to inflation asymmetry and uncertainty based on the professional forecasters’ survey data on inflation. A few studies explicitly analyse the relevance of inflation asymmetry on monetary policy formulation (Andrade et al., 2012; Evans, Fisher, Gourio, and Krane, 2016). Further, there exist several studies that discuss the causality and reverse causality between the level of inflation and inflation uncertainty (Cukierman and Meltzer, 1986; Sharaf, 2015; Su, Yu, Chang, and Li, 2017).

According to Friedman (1977), higher average inflation causes uncertainty about future monetary policy responses, resulting in broad differences in actual and expected inflation, and therefore, leads to economic inefficiency making it detrimental to growth. This relationship was later formalised in a game-theoretic framework by Ball (1992) and the work is known as the Friedman-Ball hypothesis. On the contrary, Pourgerami and Maskus (1987) argue that inflation and inflation uncertainty have a negative relationship and reject the hypothesis of the deleterious effect of high inflation on price predictability as elevated inflation levels lead to the deployment of additional resources for lowering projection error resulting in better forecasts and hence reduction in inflation uncertainty.

Coming to another dimension of a causal link from inflation uncertainty to inflation, Cukierman and Meltzer (1986) postulate that increased inflation uncertainty causes inflation to increase – the Cukierman-Meltzer hypothesis. When policymakers act with low credibility, the ambiguity of goals and poor quality of monetary control, then it may lead to an increase in the average inflation rate (Rojas, 2019). The flip side of this hypothesis is proposed by Holland (1995) who concludes that higher volatility of inflation reduces price levels reflecting policy makers’ motives for stabilisation. Further, sometimes the bidirectional relationship between inflation and inflation uncertainty is also observed under the Friedman-Ball hypothesis and the Cukierman-Meltzer hypothesis – higher inflation will increase the inflation uncertainty and vice-versa. In the case of India, Chowdhury (2014) finds evidence in support of this hypothesis using the generalised autoregressive conditional heteroscedasticity (GARCH) model. Kundu, Bhoi, and Kishore (2018) also present similar evidence between inflation and inflation volatility graphically at the sub-national level.

Inflation uncertainty is a major concern for the monetary authority, as it assigns weights inter-temporarily to minimise its loss preference. Although not explicitly, a few studies have shown the detrimental effect of high inflation uncertainty on economic activity (Sauer and Bohara, 1995; Zhang, 2010). Hence, it becomes imperative for the monetary authority to reduce inflation uncertainty through appropriate policy instruments (Gan, Yee, Hadi, and Jalil, 2019; Zhang, 2010). In a standard monetary policy rule, besides output gap and inflation, studies have included exchange rate, global policy rate, and global economic growth to examine their impact on the monetary policy rate (Hutchison, Sengupta, and Singh, 2010; Reserve Bank of India, 2021). However, there are very few studies that explicitly model inflation uncertainty in the monetary policy rule to estimate its impact (Andrade et al., 2012).

This paper adds to the limited literature in the Indian context on the importance of tail risks of inflation and their role in monetary policy. In this paper, we derive the conditional distribution of inflation based on the quantile regression in an NKPC framework that incorporates the macroeconomic environment. Further, we examine the role of distributional asymmetry and uncertainty in the monetary policy formulation. Our results support the causality between inflation and inflation uncertainty.

III. Empirical Analysis

III.1. Stylised Facts

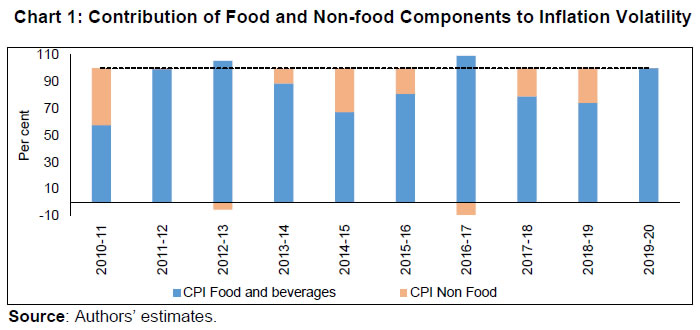

The uncertainty around food price inflation spills over to the uncertainty around headline inflation as food is a major contributor to CPI headline inflation variance (Chart 1)3. Within the FIT framework, price stability – avoiding high inflation rates or very low inflation rates over time – is the primary mandate for the RBI as volatile prices distort the economy’s price signals and may result in the misallocation of resources.

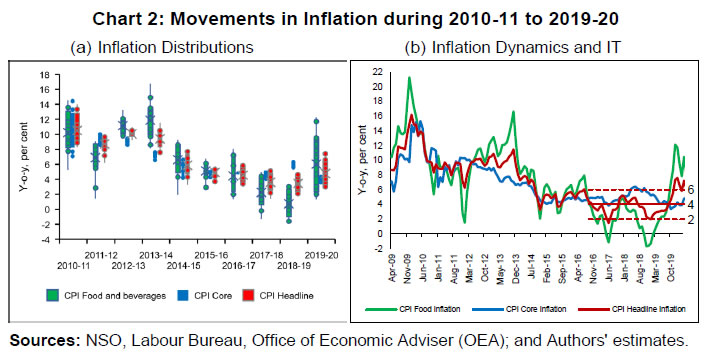

The CPI-C headline inflation has undergone significant changes in its distribution over the last decade in line with the evolving macroeconomic conditions (Chart 2a). Too high or too low inflation representing the upside and downside tail risks to inflation, respectively, is detrimental to RBI’s secondary objective of growth as well, and thus, requires a proper assessment of these risks. The FIT period coincided with a moderation in CPI inflation on the back of consecutive years of bumper food grains and horticulture production and relatively stable global commodity prices, particularly the crude oil. Irrespective of the broad easing of inflation, headline inflation deviated from the target, and went once below the lower bound of 2 per cent (in June 2017) and above the upper bound of 6 per cent consistently during December 2019-December 2020 mirroring the developments in food prices primarily owing to monsoon-related shocks and the COVID-19 pandemic-related supply disruptions (Chart 2b).

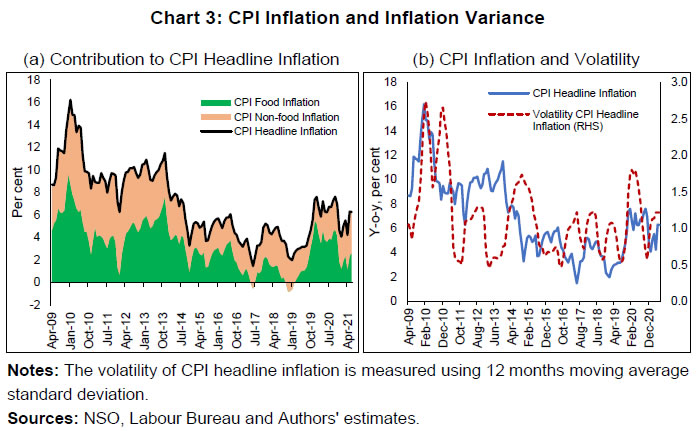

Given the high weight of food in the CPI basket, which is susceptible to adverse supply shocks, pressures in the food basket not only drives up the CPI headline inflation but also contributes substantially to its variance (Chart 3a and Chart 1). High levels of CPI inflation are often accompanied by higher volatility (Chart 3b). High inflation rates accentuate concerns about future inflation as they have the potential to influence long-term interest rates and generate uncertainty about the future value of the investment, savings, wages, tax rates, etc. In light of the fact that price stability is the primary objective of central banks, the volatility around the inflation path warrants the attention of the monetary authority. The asymmetry of distribution assumes greater importance given the fact that economic agents’ expectations are influenced by the distribution of the realised inflation (RBI, 2021).

III.2. Data and Summary Statistics

This paper uses the monthly CPI-C inflation rate (y-o-y, per cent) from September 2009 to December 2019 (before 2011, CPI-IW (CPI Industrial Workers) is used). Table 1 presents the summary statistics of variables used in the paper. The CPI-C inflation averaged around 7 per cent during the sample. It remained above average during 2010-2012. It moderated subsequently to around 4 per cent with RBI’s formal adoption of the FIT framework in 2016, which was preceded by a transitional glide path from 2014-15. The one-year ahead median inflation expectations of households have been used as a proxy for a forward-looking measure of inflation expectations4 which averaged around 11.33 per cent during the sample. As households’ inflation expectations are observed quarterly, a cubic spline methodology has been employed to convert it into a monthly series (Stuart, 2018). Given the fact that the inflation expectations series is relatively persistent and stable, the above methodology might be a better approximation to obtain monthly frequency data.

GDP growth at the constant market price has been used as a proxy for demand conditions in NKPC estimation (Banerjee et al., 2020). For real GDP growth, a similar methodology has been applied to adjust for the index of industrial production (IIP) and Purchasing Managers’ Index (PMI) composite indicator for India, which are observed every month and are coincident indicators of economic activities (see details of this interpolation in Appendix A2). In addition to these variables, NKPC estimation has been augmented with exchange rate, global commodity prices, financial conditions and global demand conditions to explain the inflation dynamics. On an average, the rupee has depreciated by 4 per cent vis-a-vis USD over the sample period with a very high degree of volatility. Commodity prices have been captured through Indian basket crude oil prices and global non-fuel commodity prices published by the IMF.

To account for financial conditions, Citi financial conditions index (hereafter Citi FCI) for India has been used as a proxy for financial conditions, which has a relatively better forecasting power in predicting real economic activity (Hatzius et al., 2010). The Citi FCI consists of a weighted average of the following variables: corporate spreads, money supply, equity values, mortgage rates, the trade-weighted dollar, and energy prices. A higher value of Citi FCI indicates easy monetary conditions, and a lower value indicates a tight financial condition. To incorporate global demand, US real GDP growth has been considered.

Moreover, we also analyse the importance given to inflation uncertainty and its distributional asymmetry in monetary policy formulation. For this purpose, the weighted average call rate (WACR) has been used as a proxy for the monetary policy rate. WACR is the operating target of the monetary policy, which is stable and symmetrically distributed at around 6.7 per cent.

Table 1: Summary Statistics

Variables

N

Mean

Std. Dev.

Median

Kurtosis

Skewness

CPI-C Headline Inflation

124

6.99

3.36

5.92

2.51

0.52

1-year Ahead Median Household Inflation Expectations

124

11.33

2.47

11.18

1.8

0.25

Real GDP Growth Rate

124

6.48

1.973

6.22

6.3

1.27

Exchange Rate Growth Rate

124

3.99

7.47

3.36

2.87

0.52

Crude Oil Price Growth Rate

124

5.81

32.45

3.2

2.82

0.3

Global non-fuel Price Index Growth Rate

124

2.22

13.88

-1.4

2.73

0.73

US Real GDP Growth Rate

124

2.16

0.95

2.2

12.25

-2.12

Citi FCI

124

-0.39

0.38

-0.46

3.11

0.67

WACR

124

6.76

1.43

6.72

3.34

-0.51

Notes: For definitions and sources, please see Appendix Table A1. Source: Authors’ estimates.

III.3. Methodology

The paper uses quantile regression to estimate the upper and lower tail risks. In a quantile regression, the quantiles of the dependent variable are explained by the set of explanatory variables. In an ordinary least square (OLS) regression, the estimated relationship is the average relationship between dependent and explanatory variables, whereas in the case of quantile regression the estimated relationship is for different specified quantiles. Thus, the benefit of using quantile regression is to estimate the role of explanatory variables in explaining extreme observations (or extreme quantiles) of the dependent variable. Since the study focuses on tail risks of inflation, quantile regression is an appropriate methodology to estimate the tail risks. Putting the quantile regression model more formally, for a dependent variable y explained by realised vector x, the quantile regression for pthquantile is given by,

In the later part of the paper, the conditional distribution has been estimated by minimising the sum of squares of the distance between the estimated quantiles from the quantile regression and quantiles derived from theoretical skewed distribution. The reason behind considering a skewed distribution is to provide space for the possible asymmetric feature of the conditional distribution. The paper considers a skewed normal distribution to estimate the smooth conditional distribution with asymmetric properties. The skewed normal distribution with parameters µ, δ, α, is given by

IV. Results

IV.1. Conditional Distribution and Tail Risks

For analysing the tail risks, the paper considers four domestic factors: one-year ahead households’ inflation expectations based on the RBI survey; real GDP growth; exchange rate vis-à-vis US dollar; and crude oil prices. In addition to this, we have also examined the impact of financial conditions and the role of FIT on tail risks of inflation in the aftermath of its implementation.

All the variables have been incorporated in the form of year-on-year percentage changes in the equations except inflation expectations (which already reflects y-o-y change) and Citi FCI. The FIT framework has been incorporated into the model through a dummy variable which takes the value of 1 after August 2016, and 0 otherwise5. The results of quantile regression are shown in Chart 4. The one-year ahead median household inflation expectations play a crucial role in CPI headline inflation dynamics.

The impact of the inflation expectations is relatively less on lower tail risks and gradually increases for higher quantiles. The domestic real GDP growth has an impact on CPI headline inflation till the third quantile. The exchange rate has a positive effect on tail risks of inflation and a very limited effect at the median level though not significant. However, a time-varying plot of coefficients of exchange rate reveals that it broadly remained significant during 2015-2018 (Appendix Chart A4).

The crude oil price has an impact on the median level and upper tail risks of inflation. Easy financial conditions have a positive influence on tail risks of inflation, and the sensitivity is relatively higher for upper tail risks. The introduction of the FIT dummy identifies the impact of FIT on CPI headline inflation tail risks. A negative coefficient of this dummy supports the success of the FIT framework. Since inflation was on a falling trend even before FIT adoption in India in 2016, the lower as well as the upper tail risks have come down by 3 percentage points.

We estimate the tail risks of inflation based on the estimated parameters of domestic and global determinants of inflation. The tail risks are conditional on historical sample data with 5 per cent tails both in lower and upper tails. The lower tail risk (l(0.05)) is considered as a measure for downside risks to inflation, and the upper tail risk (u0.95) is considered to be upside inflation risks. The estimated tail risks are shown in Chart 5. The upper tail risks of CPI headline inflation fell to a level of around 7 per cent in 2019 from a level of 15 per cent in 2010. Similarly, the lower tail risks also went down to around 2 per cent in 2019 from 8 per cent in 2010. The downward shift in inflation tail risks could be partly attributed to the success of FIT and central bank credibility (Ayres et al., 2014). Importantly, the upper tail risks fell till 2016, and they remained around 7 per cent afterwards, whereas the lower tail risks continuously fell during the sample period. This means that during the FIT period, the downside risks were relatively higher compared to upside risks coming particularly from food reflecting successive years of bumper food grains and horticulture production.

In the scenario analysis, we set preconditions on explanatory variables that influence the inflation dynamics. For simplicity, we assume data points of December 2019 as the preconditions. Next, we consider the standard deviation of the variables for one year before, i.e., January 2019 to December 2019. Then we provide one standard deviation shock to each explanatory variable and examine their impact on the conditional distribution of inflation one by one.

RBI WPS (DEPR): 02/2023: Tail Risks of Inflation in India https://rbi.org.in/Scripts/PublicationsView.aspx?id=21627

You can get more detail in the full Banking Top 10 Trends for 2023 report. https://www.accenture.com/content/dam/accenture/final/industry/banking/document/Accenture-Banking-Top-10-Trends-2023.pdf

Updated annually, our Global Banking Annual Review offers the best of our research and insights into the global banking industry. Explore the findings from our most recent report and scroll for past years’ reports. https://www.mckinsey.com/industries/financial-services/our-insights/global-banking-annual-review

Abstract This paper examines whether statistical natural language processing techniques have been useful in analyzing documents on monetary policy. A simple latent semantic analysis shows a relatively good performance in classifying the Bank of Japan (BOJ)’s documents on its governors’ policy and the impact without human reading. Our results also show that Governor Haruhiko Kuroda’s communication strategy changed slightly in 2016 when the BOJ introduced the negative interest rate policy. This change in 2016 is comparable to the one from the transition from Masaaki Shirakawa to Kuroda. In spite of the intention, the BOJ had a misjudgment in the communication strategy.

Creation Date/NO. February 2017 17-E-011 Research Project Sustainable Growth and Macroeconomic Policy